Assessing Agricultural Health through FinTech Data - An Analytical Approach

Abedalrhman K1*

DOI:10.5281/zenodo.14523484

1* Kahtan Abedalrhman, Kanzi Business Consultant, Alkhobar, Saudi Arabia.

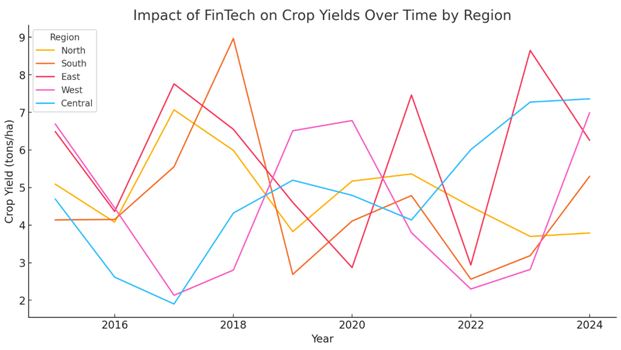

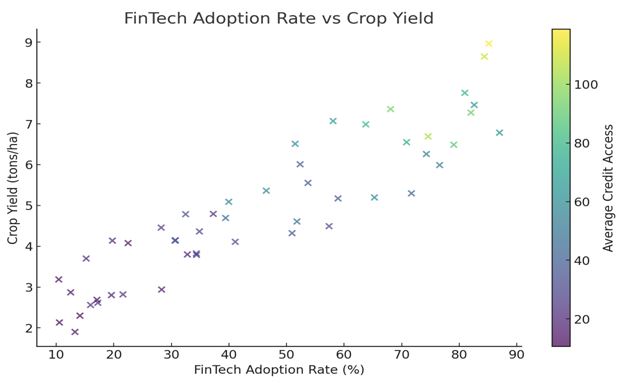

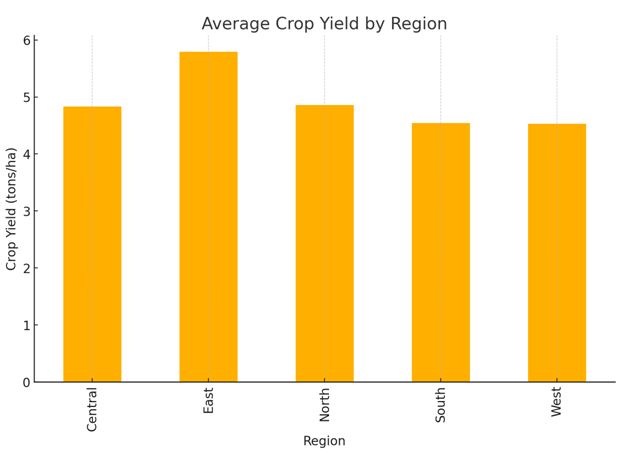

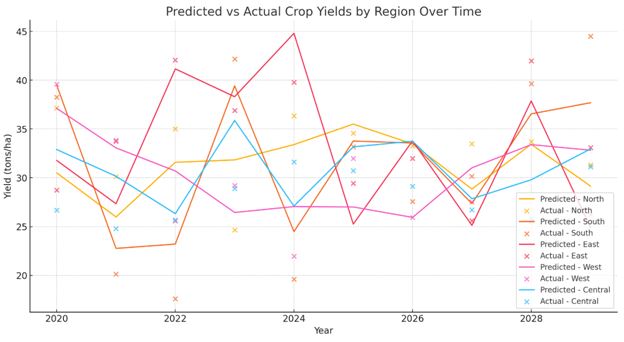

The agricultural sector plays a crucial role in the economic development of many countries, particularly those with large rural populations. However, traditional methods of assessing the health of the agricultural sector can be limited in scope and timeliness. The rapid advancements in financial technology have transformed the way financial services are delivered, particularly in rural areas. FinTech solutions, such as digital payments, lending, and insurance, can provide valuable insights into the financial activities and challenges faced by farmers and agricultural enterprises. This paper explores the transformative potential of FinTech in the agricultural sector, examining its impact on financial inclusion, resilience, and efficiency. By integrating quantitative FinTech data with qualitative insights from stakeholders, the study provides a comprehensive assessment of the sector's health. Findings indicate that FinTech complements traditional agricultural data, offering a dynamic view of financial activities and performance. Increased FinTech adoption in rural areas can drive financial inclusion, improve credit access, and foster innovation. However, challenges such as digital literacy, infrastructure gaps, and regulatory frameworks need to be addressed. The study emphasizes the importance of investments in digital infrastructure, capacity building, and collaboration between FinTech and agricultural sectors. These insights have implications for policymakers, financial institutions, and agricultural stakeholders, enabling data-driven decision-making, targeted interventions, and the promotion of sustainable agricultural development.

Keywords: fintech, agricultural sector, financial inclusion, digital finance, data analytics

| Corresponding Author | How to Cite this Article | To Browse |

|---|---|---|

| , , , Kanzi Business Consultant, Alkhobar, , Saudi Arabia. Email:  |

Abedalrhman K, Assessing Agricultural Health through FinTech Data - An Analytical Approach. Appl. Sci. Biotechnol. J. Adv. Res.. 2024;3(6):22-39. Available From https://abjar.vandanapublications.com/index.php/ojs/article/view/79 |

|

©

©